WASHINGTON (March 21, 2013) – February existing-home sales and prices affirm a healthy recovery is underway in the housing sector, according to the National Association of Realtors®. Sales have been above year-ago levels for 20 consecutive months, while prices show 12 consecutive months of year-over-year price increases.

Total existing-home sales1, which are completed transactions that include single-family homes, townhomes, condominiums and co-ops, increased 0.8 percent to a seasonally adjusted annual rate of 4.98 million in February from an upwardly revised 4.94 million in January, and are 10.2 percent above the 4.52 million-unit level seen in February 2012. February sales were at the highest level since the tax credit period of November 2009.

Lawrence Yun , NAR chief economist, said conditions for continued housing improvement are at play. “Job growth in the improving economy and pent-up demand are causing both home sales and rental leasing to rise. Though home prices are rising much faster than rents, historically low mortgage rates are still making home purchases affordable,” he said. “The only headwinds are limited housing inventory, which varies greatly around the country, and credit conditions that remain too restrictive.”

Total housing inventory at the end of February rose 9.6 percent to 1.94 million existing homes available for sale, which represents a 4.7-month supply 2 at the current sales pace, up from 4.3 months in January, which was the lowest supply since May 2005. Listed inventory is 19.2 percent below a year ago when there was a 6.4-month supply.

The national median existing-home price3 for all housing types was $173,600 in February, up 11.6 percent from February 2012. The last time there were 12 consecutive months of year-over-year price increases was from June 2005 to May 2006. The February gain is the strongest since November 2005 when it was 12.9 percent above a year earlier.

“A strong rise in home values is contributing to housing wealth recovery, which has risen by $1.4 trillion in the past year and looks to top that increase this year,” Yun said. “The extra consumer spending arising from growth in housing wealth is expected to be $70 billion to $110 billion this year.”

Distressed homes4 – foreclosures and short sales – accounted for 25 percent of February sales, up from 23 percent in January but down from 34 percent in February 2012. Fifteen percent of February sales were foreclosures, and 10 percent were short sales. Foreclosures sold for an average discount of 18 percent below market value in February, while short sales were discounted 15 percent.

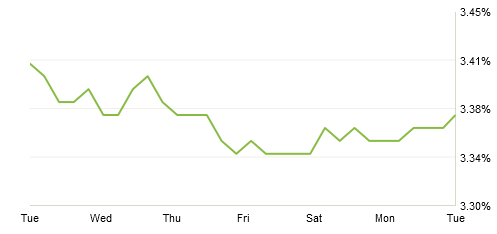

According to Freddie Mac, the national average commitment rate for a 30-year, conventional, fixed-rate mortgage rose to 3.53 percent in February from 3.41 percent in January; it was 3.89 percent in February 2012.

NAR President Gary Thomas, broker-owner of Evergreen Realty in Villa Park, Calif., said interest rates remain extraordinarily low. “In the history of mortgage interest rates since 1971, the 30-year fixed rate has been below 4 percent in only 15 months, and those have all been in the past 15 months,” he said. “Even with rising home prices, affordability remains historically favorable because home prices over-corrected during the downturn. This means there is still great value for buyers in the current market.”

The median time on market for all homes was 74 days in February, which is 24 percent below 97 days in February 2012. Short sales were on the market for a median of 101 days, while foreclosures typically sold in 52 days and non-distressed homes took 77 days. One out of three homes sold in February was on the market for less than a month.

First-time buyers accounted for 30 percent of purchases in February, unchanged from January; they were 32 percent in February 2012.

All-cash sales were at 32 percent of transactions in February, up from 28 percent in January; they were 33 percent in February 2012. Investors, who account for most cash sales, purchased 22 percent of homes in February, up from 19 percent in January; they were 23 percent in February 2012.

“There was an upward bump in the shares of investor and all-cash closed purchases in February. These sales result from purchase offers during the holidays when shopping activity by traditional home buyers slows, but investors, who typically pay cash, remained active,” Yun said. “This is a seasonal pattern, but we’re now seeing a general increase in buyer traffic, which is 25 percent above a year ago.”

Single-family home sales slipped 0.2 percent to a seasonally adjusted annual rate of 4.36 million in February from an upwardly revised 4.37 million in January, but are 8.7 percent above the 4.01 million-unit pace in February 2012. The median existing single-family home price was $173,800 in February, which is 11.3 percent higher than a year ago.

Existing condominium and co-op sales rose 8.8 percent to an annualized rate of 620,000 in February from 570,000 in January, and are 21.6 percent above the 510,000-unit level a year ago. The median existing condo price was $172,500 in February, up 13.9 percent from February 2012.

Regionally, existing-home sales in the Northeast fell 3.1 percent to an annual rate of 630,000 in February but are 8.6 percent above February 2012. The median price in the Northeast was $238,800, which is 7.6 percent above a year ago.

Existing-home sales in the Midwest slipped 1.7 in February to a pace of 1.14 million but are 12.9 percent above a year ago. The median price in the Midwest was $129,900, up 7.7 percent from February 2012.

In the South, existing-home sales increased 2.6 percent to an annual level of 2.01 million in February and are 14.9 percent above February 2012. The median price in the South was $150,500, up 9.3 percent from a year ago.

Existing-home sales in the West rose 2.6 percent to a pace of 1.20 million in February and are 1.7 percent above a year ago. With limited choices and multiple bidding, the median price in the West rose to $237,700, which is 22.7 percent above February 2012.

The National Association of Realtors®, “The Voice for Real Estate,” is America’s largest trade association, representing 1 million members involved in all aspects of the residential and commercial real estate industries. For additional commentary and consumer information, visit www.houselogic.com and http://retradio.com.

# # #

NOTE: For local information, please contact the local association of Realtors® for data from local multiple listing services. Local MLS data is the most accurate source of sales and price information in specific areas, although there may be differences in reporting methodology.

1 Existing-home sales, which include single-family, townhomes, condominiums and co-ops, are based on transaction closings from Multiple Listing Services. Changes in sales trends outside of MLSs are not captured in the monthly series. NAR rebenchmarks home sales periodically using other sources to assess overall home sales trends, including sales not reported by MLSs.

Existing-home sales, based on closings, differ from the U.S. Census Bureau’s series on new single-family home sales, which are based on contracts or the acceptance of a deposit. Because of these differences, it is not uncommon for each series to move in different directions in the same month. In addition, existing-home sales, which account for more than 90 percent of total home sales, are based on a much larger data sample – about 40 percent of multiple listing service data each month – and typically are not subject to large prior-month revisions.

The annual rate for a particular month represents what the total number of actual sales for a year would be if the relative pace for that month were maintained for 12 consecutive months. Seasonally adjusted annual rates are used in reporting monthly data to factor out seasonal variations in resale activity. For example, home sales volume is normally higher in the summer than in the winter, primarily because of differences in the weather and family buying patterns. However, seasonal factors cannot compensate for abnormal weather patterns.

Single-family data collection began monthly in 1968, while condo data collection began quarterly in 1981; the series were combined in 1999 when monthly collection of condo data began. Prior to this period, single-family homes accounted for more than nine out of 10 purchases. Historic comparisons for total home sales prior to 1999 are based on monthly single-family sales, combined with the corresponding quarterly sales rate for condos.

2 Total inventory and month’s supply data are available back through 1999, while single-family inventory and month’s supply are available back to 1982 (prior to 1999, single-family sales accounted for more than 90 percent of transactions and condos were measured only on a quarterly basis).

3 The median price is where half sold for more and half sold for less; medians are more typical of market conditions than average prices, which are skewed higher by a relatively small share of upper-end transactions. The only valid comparisons for median prices are with the same period a year earlier due to a seasonality in buying patterns. Month-to-month comparisons do not compensate for seasonal changes, especially for the timing of family buying patterns. Changes in the composition of sales can distort median price data. Year-ago median and mean prices sometimes are revised in an automated process if additional data is received.

The national median condo/co-op price often is higher than the median single-family home price because condos are concentrated in higher-cost housing markets. However, in a given area, single-family homes typically sell for more than condos as seen in NAR’s quarterly metro area price reports.

4 Distressed sales (foreclosures and short sales), days on market, first-time buyers, all-cash transactions and investors are from a monthly survey for the NAR’s Realtors® Confidence Index, posted at Realtor.org.

The Pending Home Sales Index for February will be released March 27, and existing-home sales for March is scheduled for April 22; release times are 10:00 a.m. EDT.