Prep Essential to Exterior Paint Success

Date:April 10, 2013|Category:Tips & Advice|Author:Mary Boone

Painting your house might look simple — at first glance. Look again.

Painting your house might look simple — at first glance. Look again.

Before you take on any exterior painting project, it’s important to conduct a thorough examination of your home. Here’s what to look for and how to properly prepare your home for a face-lift.

Banish mildew

Peeling, blistering and chalking are significant indicators of problems with your house paint. Water leaks will show up as discolored areas, often mildew or rot.

The experts at the Paint Quality Institute say mildew can be removed with a solution of one part bleach to three parts water. Apply the mixture to the surface, and let it sit for at least 20 minutes, applying more as it dries; rinse well. Be sure to wear eye and skin protection during this process and protect nearby plantings.

Clean the surface

Because paint won’t stick to dust or grime, you must wash your entire house, either scrubbing by hand or with a power washer. A power washer uses water from your hose and increases the water pressure as it leaves the wand to between 2,300 and 3,500 psi (pounds per square inch). In the hands of an experienced user, the power washer can be very useful. Inexperienced users, however, should know that this tool’s power can wreak havoc if it’s not used correctly. At high pressure, the water jet can etch wood, break glass and blast mortar from joints; the water also can soak the wall and requires time to dry out before painting.

Sand and patch

Once the dust and gunk are gone, you’ll need to follow up with hand scraping and sanding. On wood siding, you should fill in any gouges or holes with an exterior-grade patching compound, or “plastic wood.” Larger damaged areas should really be replaced with new siding. Cracks, seams and gaps will need to be caulked with a top-quality, paintable exterior caulk. Be sure to caulk the spots where siding meets windows and doors, corners and the edges of exterior trim.

Cover edges, trim

Next, mask off areas that you are not going to paint. You might want to place painter’s tape along the edge of house trim, and around window and door frames and trim if you plan on painting these in a different color or different type of paint. You can also tape newspaper or plastic drop cloth material over windows and doors, including sliding glass doors, to protect them from drips. Place drop cloths over plants and shrubs, or where paint may drip on porches, roof sections, sidewalks, driveways or other surfaces.

Apply primer

In order to get the best exterior painting results, it’s often necessary to use a primer or sealer before applying the paint. Primers help paint adhere better to the surface that’s being painted.

Experts say almost any exterior painting project will benefit from the use of a top-quality primer, but there are certain applications where a primer is essential, namely, when painting new wood, bare stucco or any surface that has not been previously painted. You should also use a primer when repainting an uneven or deteriorated surface or a surface that has been stripped or is worn down to the original material.

If this list of sounds extensive, it is; preparation can amount to 50 percent or more of the time it takes to paint a house. But it’s crucial; a quality job done with proper preparation and quality materials will last seven to 15 years.

Hiring a pro

If painting your home’s exterior is beyond your scope of expertise — or the project will take longer than you’re willing to invest — hire a pro to do the job. To ensure you’re hiring a reputable paint contractor, meet with a number of contractors personally and ask these questions:

- What materials do they plan to use? Who specifies the paint — you or the contractor? If the contractor selects the paint, does he or she recommend top-quality paint?

- Ask for — and check — references. Ask these previous customers if they were pleased with their work and how the paint job is performing. You may even want to take a look at their homes to see the results for yourself.

- Ask if the contractor is licensed, bonded and insured (ask to see their certificate of insurance). How many years has the company been in business? Is the business affiliated with an industry trade association? Call the Better Business Bureau to make sure there are no complaints against the business.

- Ask about payment terms. Don’t pay for work before it’s done.

- Get it in writing. The bid should include specifics about surface preparation, how shrubs and plantings near the house will be protected, the exact paints to be applied, payment terms and more.

Related:

The competition has been most intense in California, where 9 out of 10 homes sold in San Francisco, Sacramento and cities in Southern California have been drawing competing bids.

The competition has been most intense in California, where 9 out of 10 homes sold in San Francisco, Sacramento and cities in Southern California have been drawing competing bids.

Susan and Dave Edwards lost their home to foreclosure in 2010. Just two years later, they have bought a new place.

Susan and Dave Edwards lost their home to foreclosure in 2010. Just two years later, they have bought a new place.

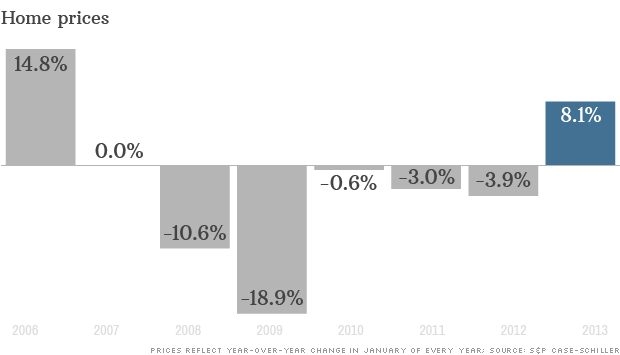

Home prices posted their biggest gain since 2006 in January.

Home prices posted their biggest gain since 2006 in January.